Take A Chance On Me

Take A Chance On Me

A Guide to Music IP Investing (Part 1)

“Having raised £231 million today and over £625 million since our IPO a little over a year ago, Hipgnosis has been one of the biggest fund launches on the London market in recent times, with more capital raised over the last six months than any other London listed fund. This is a demonstration of the financial community recognizing the true value of music and proven songs. They are the currency that makes the world go round. They are predictable and reliable and they are better than gold or oil.” – Merck Mercuriadis, CEO of Hipgnosis Songs Limited[1]

In the following three-part series, we will dive into the world of music intellectual property investing. I will provide third party data and analysis, and also draw on my own personal experiences after researching the industry, and working with investors and other industry participants.

In Part 1, we will provide a summary of the legal rights that allow music intellectual property (“IP”) owners to be financially compensated for their work. The basics of music IP are complex, but important to understand before discussing the investment opportunity.

In Part 2, we will review the current state of the global music market and the dynamics impacting music royalty cash flows. We will look at the music industry’s growth drivers and the impact of COVID-19 on the industry. We will also discuss recent M&A and capital markets activity.

In Part 3, we will dive deeper into why music royalties are considered an attractive asset class in the current market environment. We will review the main levers that active investors use when attempting to increase the value of their music IP. Finally, we will highlight ways to invest in music IP and some potential pitfalls to look out for.

_______________________________________

Part 1: What is music intellectual property?

In this first part of the series, we will look at the two copyrights associated with music intellectual property: 1) the sound recording and 2) the musical composition. We will discuss the different royalties derived from these copyrights. Next, we will review the role of record labels and publishers – the businesses that identify and finance talented artists and songwriters, and then help them create, market, and license music IP. Finally, we will review how music income flows from consumers to rightsholders. As a friendly warning, this first article may be dense for beginners and yet too basic for seasoned pros. This overview is intended as an introduction, and is only scratching the surface of these topics.

Defining Music Intellectual Property

Music royalty payments are derived from the underlying intellectual property rights of a song. Intellectual property (“IP”) is any product of the human intellect that the law protects from unauthorized use by others.[2] The most common types of IP are copyrights, trademarks, patents, and trade secrets. Music – including the lyrics, composition, and sound recording – is protected under copyright law.

A music copyright is created once put in tangible form (e.g. recorded, written in sheet music, etc.) with further protection under the law once the work is registered with the U.S. Copyright Office. A copyright provides its owner(s) with exclusive rights for a period of time. In general, the rights last for 70 years after an author’s death.

Each song contains two copyrights:

1) The sound recording copyright is a “fixation of series of sounds” associated with the particular recording by the artist(s).[3] The sound recording copyright is owned by an artist, who often assigns the copyright ownership to a record label. In return, the record label represents and manages the performing artist and its copyrights.

2) The musical compositioncopyright is the song’s composition (music and lyrics) by the songwriter(s). The musical composition copyright is owned by a songwriter, who often assigns copyright ownership to a music publisher. In return, the publisher represents and manages the songwriter and its copyrights.

The Music Royalty Framework

Royalty payments are the method through which all players (e.g. artist, songwriter, label, publisher, etc.), who are involved with the creation and sale of a song make money. There are different types of royalties paid to rightsholders, depending upon how the song is used. The licensing framework is complex, and consists of three primary royalty types.

1) Performance royalties are owed whenever a song is performed. Examples include radio, TV, online streaming services, and live venues. Musical composition performance royalties are paid by performance rights organizations (“PROs”) and collection societies. Sound recording performance royalties are paid to the artist and labels either directly or through collections societies. Importantly, in the US, whereas songwriters and publishers do get paid for terrestrial AM/FM radio, artists and labels only get paid on digital performances (e.g. satellite/online radio, interactive streaming, etc.) and not by terrestrial radio.

2) Mechanical royalties are owed whenever a song is manufactured onto a CD, downloaded on a digital music site such as iTunes, or streamed through an interactive service such as Apple Music or Spotify. Musical composition mechanical rights are typically paid by a publisher or collection agency such as the Harry Fox Agency. Sound recording mechanical royalties are paid by record labels. In the US, musical composition mechanical royalty rates are regulated by the Copyright Royalty Board, whereas sound recording mechanical royalty rates are negotiated in the free market between labels and distributors (e.g. Spotify, Apple, etc.). As a result, record labels and artists receive much higher per stream royalty rates than those of publishers and songwriters.

3) Synchronization royalties are owed whenever a song is used as background music, such as in a movie, TV program, commercial, or video game. The amount paid is negotiated in the free market between rightsholders and licensees. For rightsholders, these payments are typically less certain given their one-time nature but often quite large depending upon the use. These payments are also usually split between holders of the musical composition copyright (songwriter and publisher) and the sound recording copyright (artist and label).

The below charts from Citi Research summarizes the multifaceted music licensing framework in the U.S.[4]

Flow of Funds – From Consumers to Music IP Rightsholders

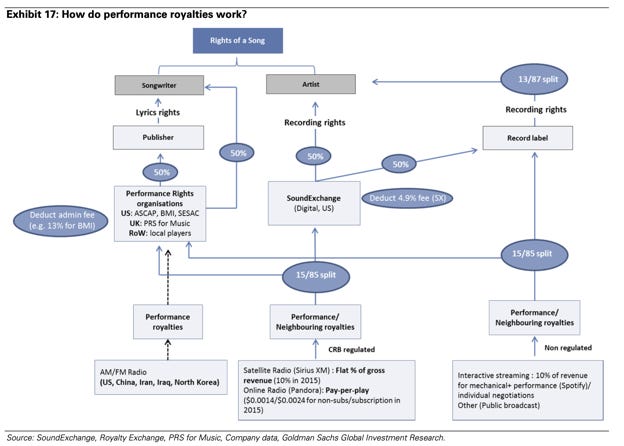

The flow of funds from the consumers of music to rightsholders can be a convoluted process. Each different type of copyright (e.g. musical composition vs. sound recording), type of royalty (e.g. performance vs. mechanical vs. synchronization) and type of use (e.g. physical CD vs. interactive streaming) work differently. Below we summarize this flow of funds and utilize some diagrams from Goldman Sachs Investment Research that try to illustrate the complexities.[5]

1) Performance royalties for the musical composition copyright are typically administered by performance rights organizations (“PROs”). Performance royalties for the sound recording copyright are paid either directly to record labels or through SoundExchange in the US.

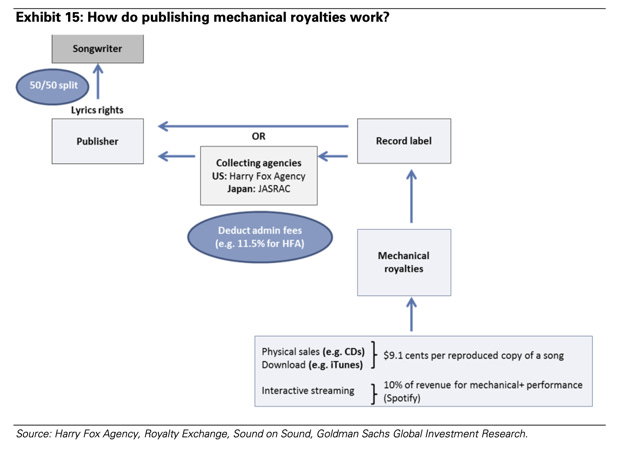

2) Mechanical royalties for the musical composition copyright are typically paid to a record label, which then pays them to the publisher directly or through an administrator like Harry Fox Agency. Interactive streaming royalties are generally paid out as a percentage of the digital services providers (“DSPs”) revenue. Mechanical royalties for the sound recording copyright are typically paid to the record label. In the US, mechanical royalties for the musical composition copyright are regulated by the Copyright Royalty Board either through a per song royalty rate basis for download/physical or a revenue share formula for interactive streaming.

Within interactive streaming, record labels are paid based on their market share with larger labels often negotiating a per subscriber minimum guarantee from the digital service providers (e.g. Spotify, Apple Music, etc.).[6] Publishers are paid based on rates determined by the Copyright Royalty Board. These publisher payments are calculated by taking the greater of a) a percentage of DSP revenue or b) a percentage of DSPs total content costs.

The per stream royalty rate varies by DSP. This dynamic exists primarily because a) each DSP has a different pricing model (e.g. free tier, family plan, premium, subscription only, etc.) and therefore a different Average Revenue Per User, and b) rightsholders are paid based on a percentage of DSP revenue regardless of the number of streams. The below chart shows the average per stream royalty rate by service in 2019.[7] Note that most DSPs pay out less than $0.01 per stream.

Importantly, with the passage of the Music Modernization Act in 2019, the administration of US digital mechanical royalties will change starting in January 2021. The legislation established a Mechanical Licensing Collective (“MLC”) to receive reports from DSPs, collect and distribute mechanical royalties, and identify musical works and rightsholders for payment. The operational costs of the MLC will be paid by DSPs.[8]

3) Synchronization royalties are more straightforward as they are typically paid directly to rightsholders by licensees, rendering a complicated chart unnecessary in this case.

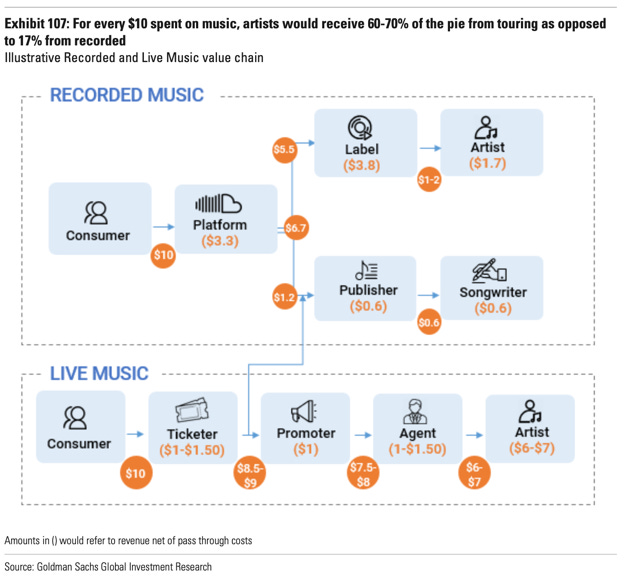

4) Touring and live music income often makes up a significant portion of recording artists’ total income. According to Goldman Sachs, artists typically generate 30% to 70% of their income from live performances. This is important in the context of COVID-19, as the pandemic has all but stopped the live music industry. We will discuss this topic more in our next article covering the current state of the music industry. Also of note, artists receive a greater percentage of the revenue generated via live performances than on streaming platforms. For every $10 consumers spend on a concert, Goldman Sachs estimates $6 to $7 goes to the artist compared to only $1 to $2 on a streaming platform.[9] This concept is reflected in the diagram below.

Now that we have a basic understanding of music royalties and the flow of funds from consumers to rightsholders, let’s discuss how record labels and music publishers work with artists and songwriters.

Record Label, Music Publisher, and Music Royalty Fund Business Models

The traditional “investors” in music IP are record labels and music publishers. Labels and publishers typically own a “catalog” of music IP rights that generate annuity like cash flows. Then, they re-invest their recurring catalog cash flows into finding and developing new music rights. As an analogy, this is similar to an oil and gas company that has many producing wells, which generate ongoing cash flow. The company reinvests its producing well cash flow into drilling new wells, so that it can continue to grow its business even further.

While not necessarily a new concept, music royalty funds have been growing in popularity over the last several years. Royalty funds primarily purchase music catalogs with a history of recurring cash flow and distribute this cash flow to its investors on a regular basis. Unlike labels and publishers, these royalty funds usually do not re-invest a significant amount of their catalog cash flow into finding and developing new artists and songwriters. Returning to our oil and gas analogy, royalty funds are not in the exploration business.

In this section, we will take a closer look at these three business model types.

1) Record labels scout, identify, and develop recording artists. They also handle marketing, promotion, distribution, and licensing of the sound recording copyrights created by their recording artists. The deal between a record label and a recording artist varies greatly depending upon size of advance, popularity of the artist, and other factors. But often, the artist assigns ownership of her sound recording copyrights created during the term of the deal to the record label. In return, the record label makes an “advance” to the artist and provides various label services with the goal of maximizing the artist’s success. This advance is a lump sum payment to the artist which is then recouped from future royalties generated by the artist’s music. Once the advance is recouped, the label typically receives 80% to 85% of future royalties with the artist receiving the remaining 15% to 20%. The relatively high percentage split to record labels illustrates the perceived risk of identifying and funding successful artists. In many ways, the artist/label deal structure reflects a participating preferred security seen in venture capital financings. But the artist/label deal often allows for the label (investor) to retain a much higher ownership percentage than is typical in a venture capital deal. The main costs for a record label are 1) artist & repertoire (“A&R”) costs associated with finding, signing artists, and recording their new music; 2) sales and marketing costs to promote music; 3) product costs to manufacture and distribute music; and 4) general overhead expenses.

For example, the figure below illustrates Warner Music Group’s Recorded Music segment’s cost structure over the past three years.[10] Roughly 35% of Warner’s Recorded Music division’s total expenses are spent on A&R to find and develop new artists.

2) Music publishers find, promote, market, and administer songwriters’ musical output. The deal between a publisher and a songwriter also varies. But just like recording music deals, the agreement often includes the songwriter assigning ownership of her musical composition copyrights created during the term of the deal to the music publisher. In return, the publisher makes an advance to the songwriter and provides various services. Once the advance is recouped, the publisher typically receives 50% of future royalties with the songwriter retaining the remaining 50%. In a “co-publishing” deal, which is common among successful songwriters, the publisher only keeps 50% of the publishing share (or 25% of future royalties), meaning the songwriter receives 75% of future royalties. The main costs for a music publisher are similar to that of a record label: 1) A&R expenses; 2) sales and marketing expenses; and 3) general overhead expenses. For example, the figure below summarizes Warner Music Group’s Publishing cost structure over the past three years.[11]About 85% of Warner’s Publishing expenses are related to A&R.

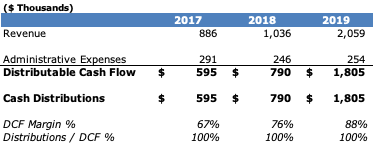

3) Music royalty funds purchase existing music royalty catalogs usually with a stable history of income. Music royalty funds do not spend much, if any, time or capital on finding and breaking new artists and songwriters. Instead, royalty funds typically acquire cash flowing catalogs from songwriters, artists, producers, and their heirs. Sometimes these funds also buy catalogs directly from publishers and record labels, occasionally acquiring publishers and record labels outright. Music royalty funds then often pass through this cash flow to their investors, making regular distributions, in a similar fashion as an oil and gas royalty or real estate investment fund might. Music royalty funds often will take an active role after acquiring a catalog by attempting to increase the catalog’s cash flow and decrease expenses. We will cover these levers in more detail in Part III of this series. The main costs for a music royalty fund are general overhead expenses related to acquiring the assets and administering them. This lower cost structure results in higher operating margins relative to record labels and publishers, but typically lower revenue growth (absent one-time settlements and acquisitions). For example, the figure below summarizes Mills Music Royalty Trust’s cost structure over the past three years. Mills Music Royalty Trust has minimal general & administrative costs, and distributes ~100% of its distributable cash flow (“DCF”) to investors. It is worth noting that the significant revenue growth in 2019 was driven by a one-time $1 million settlement for prior period royalty underpayments.[12]

Looking Ahead

As you can see, music intellectual property is a complex web of copyrights, royalties, multiple stakeholders, and business models. And, in our view, it is important to understand the legal and financial basics before investing in the asset class. It is our hope that this article provided a helpful introduction and will better equip you as we continue to dive into the space. In the next article, we will look closer at the music industry today in order to further explore the dynamics affecting music royalty cash flows.

[1] Music Business Worldwide, “Merck Mercuriadis’ Hipgnosis raises another $295 million”, https://www.musicbusinessworldwide.com/merck-mercuriadis-hipgnosis-raises-another-295m/[2] Cornell Law School, https://www.law.cornell.edu/wex/intellectual_property[3] US Copyright Office, https://www.copyright.gov/circs/circ56.pdf[4] Citi Equity Research, “Putting the Band Back Together”, August 2018.[5] Goldman Sachs Investment Research, “Music in the Air: Stairway to Heaven”, October 2016.[6] JP Morgan Equity Research, “Warner Music Group: Music to Our Ears”, June 2020.[7] Goldman Sachs Investment Research, “Music in the Air: The Show Must Go On”, May 2020.[8] US Copyright Office, https://www.copyright.gov/music-modernization/115/[9] Goldman Sachs Investment Research, “Music in the Air: The Show Must Go On”, May 2020.[10] Warner Music Group S-1, February 2020.[11] Warner Music Group S-1, February 2020.[12] Mills Music Trust 10-K, March 2020.

Excellent introduction to the world of music intellectual property investing!