A New Tune: Looking at the Future of BMI

A New Tune: Looking at the Future of BMI

Why – after 80+ years – the PRO is charting a new direction.

If you’re not already a subscriber to Leveling Up and want to join other curious music industry professionals, creators, investors, and entrepreneurs, enter your email below and you won’t miss out on future newsletters:

GM readers 👋,

Happy September!

It’s been a big month here at Alderbrook HQ! Hannah and I signed a lease and will be moving to Nashville in October. We’re going to miss our New Orleans friends & family a lot, but we’re excited about this next chapter. Finally, I’ll be in the LA area during the week of October 23rd for the Music Tectonics conference. Shoot me an email or fill out a meeting form (linked here), if you’d like to grab a coffee – I’d love to catch up!

I’ve added a new section to the end of this month’s newsletter. In it, I share some of my favorite content from the past month. There are a lot of smart folks on the internet generating a ton of amazing content. I hope you find these articles and podcasts as insightful as I do!

For this month’s post, instead of writing about music catalog M&A or some hyper-growth music tech start-up or trend, we’ll be covering Broadcast Music Inc. (“BMI”). If you’re not already familiar, BMI is an ~84 year-old licensing organization with slow but steady growth.

Admittedly, “slow and steady growth” is not one of the most exciting phrases in the English language. But stay with me – don’t close that tab yet! There are interesting angles to this story.

In the past 12 months, BMI has made two big strategic decisions – 1) becoming a for-profit and 2) considering a sale to a private equity firm – that have been controversial to say the least. Some in the songwriting and music publishing community (i.e., BMI’s customers) are questioning the company’s intentions and how its moves will impact them. Others are openly angry, publicly calling BMI executives “greedy”.

In light of the latest buzz, let’s try to understand what is driving BMI’s strategy as best we can. I’ll also share my two cents on the potential drivers of value for a private equity buyer. And I’ll wrap up by weighing the implications of a sale on various stakeholders.

And with that, on to the disclaimers…

Note: I write this newsletter to learn in public. I’m not a licensed investment professional. This piece is for informational purposes only. None of this is tax, investment, or legal advice. Do your own research!

Now, let’s get after it!

Jimmy

A New Tune: Looking at the Future of BMI

“The entrepreneur is the customer and the LP is the shareholder. That’s the only way to think about the venture capital business that makes sense to me.” - Fred Wilson

Back in 2010, I stumbled across legendary venture capitalist Fred Wilson’s blog – avc.com. At the time, I hadn’t heard of him and had little knowledge of the venture capital industry. Nevertheless, I was drawn to Wilson’s straightforward, curious, and thoughtful writing. In the years since, the blog has become one of my favorite places to learn about investing and technology on the internet. Many posts have timeless insights and lessons.

One evergreen post is “The VC’s Customer.” Published in 2005, Wilson argues that venture capitalists’ (“VCs”) ultimate customers are entrepreneurs (i.e., the people who VCs give money to build businesses) and not the VC’s limited partners (i.e., the people who give VCs money to invest). Wilson explains:

“I start with the value chain. The entrepreneur creates the value, they are the "raw material" in the venture capital business. If there were no entrepreneurs, there would be no venture capital business. So the VCs who treat the entrepreneur like the customer and invest heavily in customer service will be rewarded with the loyalty of the most important component in the value chain. Money, on the other hand, is a commodity, whether it’s in the hands of the LPs or the VCs. Money flows to the best returns and always will. So if the VC does a good job of serving his customers well and generates superior returns as a result, the money will always be there as long as the price of his fund is reasonable.”

As Wilson sees it, serving the entrepreneur well is the most important part of his job as a VC. If the VC does this well, his limited partner shareholders (“LPs”) should benefit too. Still, Wilson acknowledges that an “entrepreneur is the customer” mantra has its challenges, especially as it relates to customer relations – whether it’s respectfully handling the thousands of “customer” pitches his firm receives each year or thoughtfully delivering hard news when the “customer” is performing poorly. As a result, Wilson believes that it’s important for VCs to put in the time, energy, money, and intellect to deliver great customer service for entrepreneurs.

As I followed the news about BMI over the past year, I kept thinking of Wilson’s post. For those familiar with the music licensing space, BMI needs no introduction. But for the uninitiated, BMI is the New York City-based performance rights organization (“PRO”) founded in 1939 by the National Association of Broadcasters (“NAB”), a trade and lobbying group for the radio and TV industry. Today, BMI is the largest U.S. PRO by revenue and distributions to songwriters & music publishers!

But more recently, BMI has been making music industry headlines for its controversial strategic moves. In March 2022, reports emerged that BMI had hired investment banking firm Goldman Sachs to explore the organization’s ‘strategic options’. Then in October 2022, after operating broadly on a not-for-profit basis since it was founded in 1939, BMI decided to change to a for-profit model. Finally, in August 2023, the company was reportedly talking to private equity firm New Mountain Capital about a $1.7 billion sale.

This was followed by various songwriter groups sending a letter to BMI’s CEO Mike O’Neill, with 18 questions seeking greater transparency on the company’s moves and how they might impact songwriters and publishers in the future. O’Neill’s reply didn’t provide many details on the company’s recent moves. For example, according to O’Neill, the move to a for-profit business model was made, so that BMI “could invest in our company to ensure our continued success and growth for the future, while also increasing our distributions.” Meanwhile, O’Neill claimed the potential sale would enable BMI “to invest in our business and explore new avenues for revenue generation so we can continue to expand our distribution sources.” O’Neill’s reply left BMI’s concerned songwriter groups “extremely disappointed” and still in search of answers.

In this piece, we’ll take a look at BMI’s current state and speculate on what could be driving these decisions. Next, we’ll consider why a private equity firm like New Mountain Capital may be interested in acquiring the business. Finally, we’ll weigh the potential implications to the various stakeholders impacted.

How is BMI faring?

To understand what is driving BMI’s recent strategic decision-making, we must first understand the organization’s mission and its business model. From BMI CEO Mike O’Neill’s recent blog post, the company’s mission is to “serve our songwriters, composers and publishers and grow the value of your music” and said mission is realized through investments “in new businesses, technologies and enhancements.” This roughly translates into a company that:

Acquires and retains songwriters, publishers, and composers (what BMI calls its “affiliates”) whose music has broad appeal. From BMI’s 2022 Annual Report: “The Company’s success is a direct result of BMI’s incomparable repertoire and its unmatched worldwide appeal.”

Plugs BMI signed musical works into as many licensed locations as possible.

Monitors usage, collects payments from licensees, and distributes payments to its affiliates. PROs, like BMI, focus specifically on the collection of performance royalties, which are owed whenever a song is performed publicly. These rights cover a wide variety of situations, so BMI is collecting from radio, TV, online streaming services, gyms, bars, restaurants, live venues, and so on.

To some degree, reports to affiliates / customers in order to provide transparency around usage and payments.

Importantly, BMI and its closest U.S. PRO competitor ASCAP must conduct business under a consent decree, an agreement between each organization and the U.S. government which lays out the rules under which the PROs do business. Among other things, the consent decree requires BMI to accept any writer who wants to join and requires royalty rates to be set by a U.S. court (“rate court”) rather than negotiated in the free market. Several of BMI’s smaller PRO competitors – like SESAC and Global Music Rights – are not subject to a consent decree, which means these companies can be selective in accepting new members and can potentially negotiate higher rates from licensees who want to use their customers’ music.

How has the above strategy been working? In short, extremely well. Between 2003-2022, it has resulted in sustained and consistent business growth.

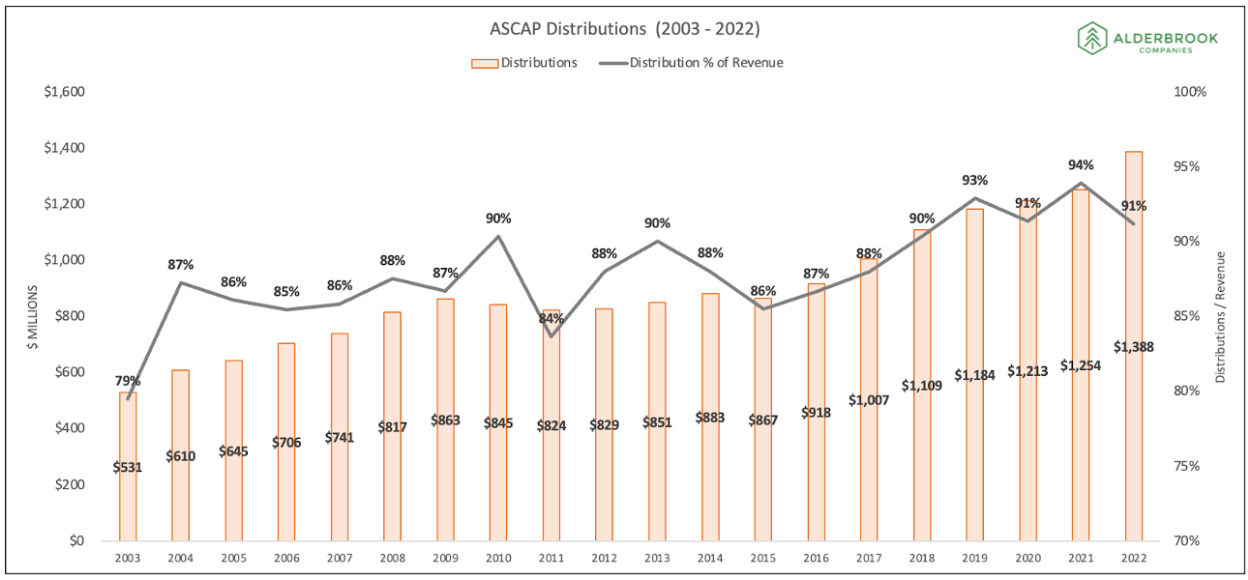

On the financial side, the growth of annual revenue has been consistent through various economic recessions and has accelerated in the past two years. BMI has grown revenue at a ~5% compound annual growth rate (“CAGR”) since 2003 with revenue increasing every year except for one (2012). And 2022 saw BMI achieve its fastest annual growth at ~12% year-over-year. Meanwhile, the company has gradually increased the percentage of revenue it distributes to its affiliates. For example, whereas BMI distributed songwriters and publishers 86% of its revenue in 2003, the company distributed 94% of its revenue in 2022!

So as not to view BMI’s growth in a vacuum, let’s compare it to its biggest competitor ASCAP. As the charts below show, BMI has grown at a slightly faster CAGR (4.9% vs. 4.4%) between 2003-2022 and currently distributes a higher % of revenue (94% vs. 91%). On the financial side at least, BMI appears to be slightly outperforming its primary competitor in aggregate.

On the customer side, BMI’s affiliates continue to grow at a consistently high single digit rate, which clearly showcases the value of the business to the songwriting and publishing ecosystem. While I couldn’t find any data on BMI’s retention rate, I’d guess it’s very high (i.e., 90%+), given its consistent affiliate growth and the fact that its competitor SESAC’s retention rate is reportedly 99.7% since 2003. That said, BMI’s average revenue per affiliate (~$1,200 currently) is declining and significantly less than that of competitors like SESAC ($7,000+), which are not subject to regulated royalties stemming from the consent decree.

And finally on the engagement side, BMI has seen its annual number of licensed performances increase exponentially since 2014, reaching 2.23 trillion performances in 2022. The 4.5x increase in performances underscores the increasing demand for BMI’s repertoire.

Overall, BMI’s high-level business metrics look quite healthy from my perspective. I can’t think of too many businesses that generate $1+ billion of revenue, grow consistently in the mid-single digits regardless of economic climate, and produce operating margins that enable it to distribute out 90%+ of its revenue.

Why is BMI making strategic changes?

Given the above context, we must be missing something. Otherwise why would BMI shift its business model to for-profit status and explore a sale? Why would BMI’s CEO express the below concerns around the company’s future prospects?

“It is easy to assume that if we kept doing business the way we always had, distributions would continue to grow. That is a dangerous assumption to make, because in an evolving industry like ours, you run the risk of settling for a larger slice of a shrinking pie. Our goal is to grow that pie to your benefit...And let me address the speculation about a potential BMI sale. While we have the resources to continue to grow our business, if we can find a partner who can help us take advantage of new opportunities and provide a new level of investment and technological expertise, then of course we would explore that.”

I see three potential drivers of BMI’s strategic changes. As discussed, BMI hasn’t been entirely direct about the details surrounding their moves, so I’m admittedly speculating here.

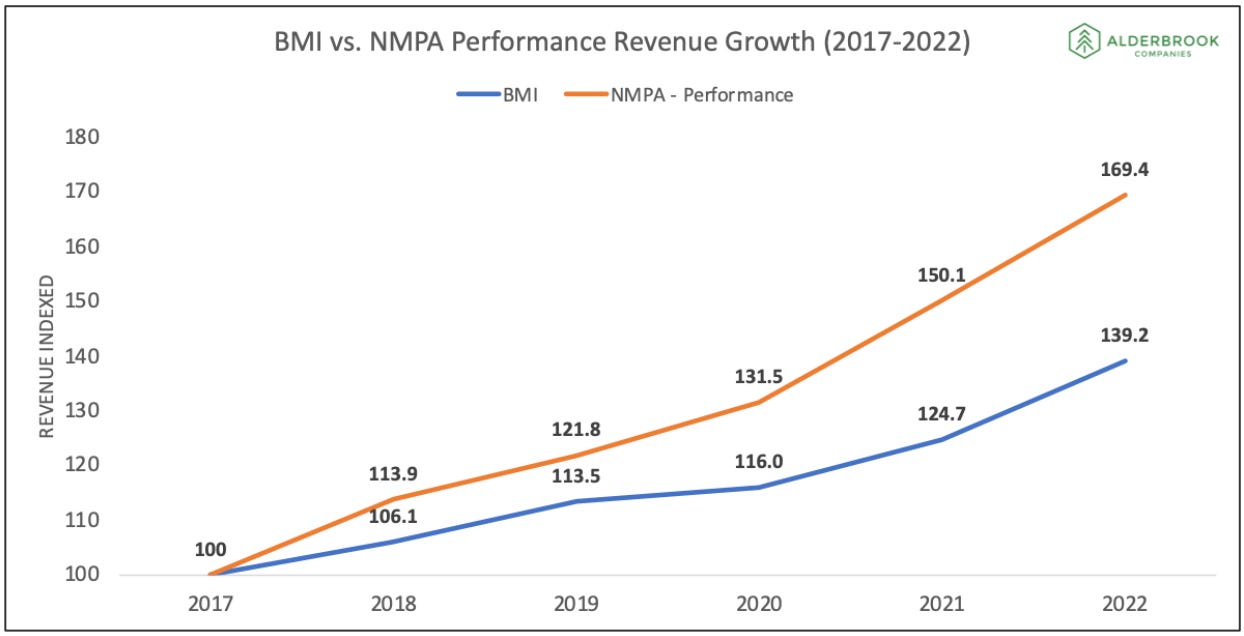

BMI’s performance rights revenue is growing slower than the U.S. industry average. According to the National Music Publishers’ Association (“NMPA”), U.S. performance revenue increased at an 11% CAGR since 2017 versus a 7% CAGR for BMI and 6% CAGR for ASCAP over the same period. This suggests that smaller U.S. PROs like SESAC and Global Music Rights are stealing market share from their two largest rivals. By making greater investments in technology and customer service, BMI can potentially strengthen their position in the U.S. PRO market and arrest their market share losses. Along these lines, the company recently announced a new customer service initiative to improve its technology, systems, and processes that handle royalty and administration questions from BMI’s affiliates. BMI clearly believes that its recent strategic moves will support greater investment in services like this.

Source: BMI and NMPA U.S. performance rights income is growing slower than other right types. BMI’s business performance is currently driven by the health of the performance rights market, which is growing slower than other right types. For example, the NMPA reports that U.S. performance revenue has grown at an 11% CAGR since 2017 vs. synchronization income growth of 19% and mechanical revenue growth of 16% over the same period. Along these lines, in 2022, performance royalties made up less than 50% of NMPA revenue for the first time in history. This may be what BMI CEO Mike O’Neill is referring to when he says there is a “shrinking pie.” As a result, BMI may want to diversify its collections business by revenue source and gain exposure to faster growing royalty types like mechanical and synchronization royalties. It may see a for-profit structure combined with additional capital from a new owner as the best way to execute this. As a reminder, PRO competitor SESAC (which is owned by private equity firm Blackstone Group) has run a similar playbook with its acquisition of Harry Fox Agency, which focuses on the administration of mechanical royalties.

Source: NMPA Finally, BMI’s shareholders and management team may want to maximize their economics right now. It’s hard to know how BMI’s decision makers are incentivized because the company is private. Its ownership structure and executive compensation plans are unknown. However, it’s worth noting that BMI’s board of directors (pictured below) consists mainly of radio and television executives.

Source: BMI If we assume BMI’s board is reflective of its current shareholder base, it suggests that these “legacy media” companies will receive the proceeds from the reported $1.7 billion sale of BMI to a private equity firm. For smaller companies like Beasley Media Group (market capitalization of less than $30 million) and Urban One Inc (market capitalization of less than $300 million), these proceeds could be quite meaningful relative to their current equity valuations. For example, every 1% of BMI equity ownership likely equates to ~$17 million of proceeds to shareholders. Similarly, BMI’s management team may benefit financially from a sale and receive future incentives (e.g., stock options in the company) from a private equity buyer to continue growing the business. Again, we don’t have any details here, but these considerations could certainly be contributing to BMI’s recent strategic decisions.

All in all, BMI’s core business metrics appear quite healthy right now, so it seems strange for the company to be making major strategic changes. That said, the company’s recent results don't look quite as attractive in the context of broader industry trends. BMI’s performance revenue isn’t growing as fast as the industry and that’s likely a result of increased competition from smaller PROs. Meanwhile, other income types – like mechanical and synchronization – are growing more quickly than performance royalties, which is BMI’s current focus, so the company may want to diversify its exposure by income type. Finally, there are likely attractive economic incentives for BMI’s shareholders and team in pivoting to a for-profit model and potentially selling the business.

Why is private equity interested in BMI?

Now that we have at least a few ideas as to why BMI is exploring a sale, let’s analyze why a private equity firm like New Mountain Capital is reportedly willing to pay ~$1.7 billion – 12x BMI’s last twelve months’ of EBITDA – to acquire the company.

As background, the private equity playbook typically involves three levers to make money in a transaction:

EBITDA Growth: Private equity (“PE”) firms look to increase a target companies’ profitability as measured by their earnings before interest, taxes, depreciation and amortization (“EBITDA”). PE investors often try to grow revenues through both organic (e.g., price increases, entering new markets, etc.) and inorganic (e.g., acquisitions) means. Meanwhile, they may also look to cut costs in order to improve margins. The goal is to grow EBITDA so that it is significantly higher when the PE firm goes to sell the business in the future.

Leverage. PE firms almost always look to acquire businesses with a material amount of debt. By using more debt, PE investors can increase their return on equity. As a result, they prefer businesses that generate consistent, sustainable, and substantial cash flows, which can be used to repay the debt used to acquire a target company over time.

Multiple expansion. This is also known as “buy low, sell high.” PE firms hope to be able to sell companies in the future at a higher multiple of EBITDA than where they bought in.

According to Goldman Sachs, the primary source of PE firm value creation today is operational improvements (i.e., EBITDA growth). This is quite different from the 1980s when leverage drove the majority of returns.

New Mountain Capital’s private equity strategy certainly appears to be focused on the EBITDA growth bucket. Here are the characteristics it looks for before making an investment in a company:

From my perspective, BMI checks each of New Mountain Capital’s boxes strongly, maybe with the exception of the “high barriers to competitive entry” bullet. (In my opinion, the company has low-to-medium barriers.) For example, it is a market-leading U.S. performance rights organization. It has grown consistently since at least 2003, suggesting that the industry is non-cyclical. It appears to have very high retention rates for its ~2 year standard agreements with songwriters and publishers. It currently has a “clean” balance sheet without any debt, enabling a private equity investor to more easily use leverage in a transaction. And it generates meaningful free cash flow, which is underscored by its 90%+ distribution as a percentage of revenue ratio.

Finally, it likely has several notable future EBITDA growth opportunities for a private equity firm like New Mountain Capital to focus on realizing. These opportunities include:

New market expansion. New Mountain Capital could drive BMI to expand into new geographical markets or new business categories. This could involve pursuing international growth opportunities, such as opening new BMI offices and/or using M&A to acquire PROs in fast growing music markets like the Middle East & North Africa, Southeast Asia, and Sub-saharan Africa. It could also include diversifying BMI’s revenue beyond performance royalty streams by venturing into faster growing areas such as synchronization licensing, mechanical licensing, or music data analytics. Again, this is a similar approach to what SESAC has done over time after being acquired by private equity investor Blackstone. Lastly, BMI could focus on building a business focused on financing writers, composers, and independent publishers – potentially starting to even acquire catalogs outright – leveraging its vast amount of historical data on performance rights.

Technology and data enhancements. A PE investor could provide BMI with the capital necessary to upgrade its technology and data analytics tools. This may potentially improve the company’s ability to track music usage and collect royalties more accurately. As a result, BMI can become even more competitive in the market, more easily attracting new affiliates / customers and retaining existing ones.

Cost management. New Mountain Capital could also look to improve BMI’s operating margins by reducing its costs. In its first year of operating as a for-profit, BMI reportedly generated $145 million of EBITDA implying a ~9% EBITDA margin. That margin is likely much lower than its smaller competitors like SESAC, which generated a ~29% EBITDA margin in 2019. I expect that New Mountain Capital will look to reduce this differential over time. While some of the margin difference is likely due to BMI’s consent decree, there may be levers to reduce costs. For example, the company reduced headcount ~10% last year and a PE buyer may look to make further cuts. BMI also distributed 94% of revenue to affiliates in 2022, which was higher than ASCAP’s 91% and significantly higher than SESAC’s reported ~50% in prior years. For a PE buyer, this may be an attractive lever, because every 1% reduction in distributions increases EBITDA ~$15 million or 10%. That said, it’s only attractive up to a point, because any significant reduction in the payout ratio could threaten the BMI’s relationship with its affiliates.

In summary, it’s not surprising that New Mountain Capital is interested in acquiring BMI. The company’s fundamentals are strong, and there are likely several avenues to grow its profitability. Future growth through any of the means highlighted above will likely require a fresh perspective and tight execution from a leadership team willing to put in the work. At the same time, a private equity buyer will almost certainly want buy-in from one group potentially overlooked in the formulation of the investment case – BMI’s affiliates (i.e., songwriters and publishers).

What are the implications?

The implications of BMI’s new for-profit model and potential sale to private equity will likely impact various stakeholders in different ways. From my perspective, participants will be impacted as follows:

BMI’s management team. BMI’s executives will likely have an easier time executing their vision for the company under a for-profit model and with private equity ownership. In this scenario, BMI’s team will now have more flexibility and greater resources to make the investments that it feels are necessary to remain competitive and grow over time. From BMI CEO’s recent blog post: “That’s why we changed our business model last year to both invest in our company and grow your distributions in ways our old model prevented us from doing…if we can find a partner who can help us take advantage of new opportunities and provide a new level of investment and technological expertise, then of course we would explore that.” In addition to having more resources, BMI’s team will likely have the opportunity to earn greater compensation in the new model versus the old one. Studies have shown that for-profit executive salaries are at least 25% higher than those of non-profits. Furthermore, private equity firms almost always incentivize executive teams with equity options / ownership in their companies, likely enabling BMI’s team to have upside in the company’s future value for the first time (assuming the team does not already have an ownership stake after converting to a for-profit).

BMI’s current shareholders. In early 2022, BMI was a not-for-profit enterprise. As a result, its shareholders didn’t necessarily own a highly valuable economic interest. Now, BMI’s current shareholders will reportedly receive ~$1.7 billion if the company is sold. While I don’t know the price BMI’s shareholders paid for their current ownership stakes, my sense is that the cost was negligible when converting from a not-for-profit to a for-profit business. All in all, that sounds like a big win for its current shareholders!

BMI’s songwriters and publishers. As discussed, BMI’s affiliates are concerned about the company’s recent changes. Based on what’s currently public, BMI’s affiliates aren’t going to receive any proceeds from the company’s sale. And while they may benefit from investments in BMI’s technology, data, and reporting capabilities, it’s not surprising that they are asking if a sale to a private equity firm is the best way to accomplish these goals. If BMI were to be sold to a PE firm, it could potentially create conflicts of interest and raise various concerns, particularly considering the unique mission and role of PROs like BMI in the music industry. For example, PE firms seek to maximize returns for their investors. This focus could conflict with BMI's original priority of advocating for fair rightsholder compensation and distributing them this compensation. Of course, BMI will still be incentivized to keep affiliates happy, but the changes will introduce a competing priority of making shareholders happy. From my perspective, BMI’s songwriters and publishers may benefit from these strategic changes in the intermediate- to long-term if the company’s long-term bets are successful. But the details for how and when this may happen currently aren’t available based on what the company has said publicly. And these benefits will likely take time to realize and may come at the cost of short-term pain for songwriters (i.e., cutting the distribution to revenue ratio). It’s particularly concerning that BMI will reportedly no longer report its financial results publicly, reducing transparency further. So, in addition to communicating the new vision and strategy to affiliates in greater detail, BMI may want to consider granting its affiliates a percentage of any sale proceeds and/or a percentage of the go-forward company’s option pool to more closely align incentives and generate buy-in for a transaction.

BMI’s competitors. In the near-term, I expect BMI’s rivals to benefit from these changes. ASCAP has already launched a series of marketing campaigns trumpeting its prioritization of creator interests. However, over the longer-term, BMI’s future investments may afford it a stronger position in the market by providing improved services for its affiliates.

Closing Thoughts

Today is the beginning of the new BMI. It will be important to follow how the company treats its various stakeholders during the transition process. In a decade from now, we may look back at this moment as a key turning point for BMI in its pursuit to develop better services for its affiliates and a more diversified business for its shareholders. There is the potential that these changes enable BMI to accelerate revenue and distribution growth.

But making these investments won’t be without risk. So in order to achieve its vision, the company’s leadership likely needs to lean more into transparency with its current and future affiliates – songwriters and publishers – in order to align them with this new direction.

Currently, it is clear that many BMI affiliates are worried about all this change. Will BMI’s management and current shareholders benefit the most at the expense of its affiliates? Will a new private equity owner be prioritized over songwriters and publishers going forward? Will BMI cut the distribution to revenue ratio in the future.

From my perspective, these are important questions that deserve thoughtful and direct answers.

Just like Fred Wilson highlighted in his “The VC’s Customer” newsletter, now seems like the time for BMI to focus on customer relations. I expect that BMI’s leadership wants to create alignment with affiliates. So I imagine that the BMI team will continue to focus its time, energy, money, and skill on songwriters and publishers during this transformative period. It may be a tall order with some unpopular answers, but it feels like the stakes are too high to compromise on it.

Thanks to Hannah and Adam for the feedback, input, and editing!

Leveling Up’s work is provided for informational purposes only and should not be construed as legal, business, investment, or tax advice. You should always do your own research and consult advisors on these subjects. In addition, our work may feature entities in which Alderbrook Companies, LLC or the author has invested and/or has provided consulting services.

📚 Music Business, Tech, and Investing Content Worth Consuming

Here is some of the best content that I consumed over the past month –

Taylor Swift’s Re-Records May Be Exceeding Even Her High Expectations (MBW: link)

What Will TikTok’s New Streaming Service Mean for the Industry? (Billboard: link)

Misaligned Incentives Make the Music Business a Zero-Sum Game (MIDIA: link)

TuneCore’s AI Study (TuneCore: link)

AI A Threat To Music? Try Telling That To This Artist From Costa Rica (MBW: link)

AI Generated Art Lacks Copyright Protection (Bloomberg: link)

Want to Invest In Your Favorite Song? JKBX Bets Fans Will Bring Billions to Market (Billboard: link)

ABBA Voyage Is Making $2 Million a Week With an Avatar Band (Bloomberg: link)

If I Ran Spotify - I’d Do These 8 Things (Where Music’s Going: link)

🤝 Want to Work Together? Get in touch!

Interested in working together? Here’s a reminder that Alderbrook would love to work with you!

Since 2017, Alderbrook has advised 50+ companies across various industries and stages. This includes working with record labels, music publishers, music technology companies, and investors on a wide-range of projects. Our experienced group of consultants provide services across several categories, including: a) market research; b) corporate strategy; c) investment and M&A due diligence; d) capital raising support; and e) financial planning & analysis.

In addition to the above consulting services, we also have a growing venture portfolio of 20+ early-stage investments. Our primary focus is backing founders who we believe in and whose vision we are aligned with. While we are industry agnostic, our preferred sectors are media, software, and government technology.

Finally, reach out to us about opportunities to sponsor Leveling Up’s newsletter. Our readership includes music technology entrepreneurs, executives at major labels, Grammy award-winning creators, investors and bankers at large financial institutions, and more. Share what you’re building with them!

To get in touch, you can either reply directly to this email or click the link below to fill out our contact form. We’ll be back in touch soon!

📭 Share Leveling Up with a friend!

If you enjoy Leveling Up, please consider sharing it with friends and colleagues (link to share)!